Breaking down a loan

After joining CreditPer, I had to get myself comfortable with the business side of things i.e. finance. Grasping the domain knowledge is mandatory as an engineer because the software we build revolves around that domain.

Note: The flow I discuss in this article is my limited view of how loans work. This is by no means a comprehensive (or 100% correct) flow, but just the knowledge I have gathered as of now. Plus it is related to how CreditPer handles loans, which may be different than normal flows.

I’m only discussing how the numbers are broken down. Investopedia and internet has better definitions of all the terms, so I won’t be talking about that.

Journey of a loan

By journey of a loan, I refer to the entire flow from the start of the loan i.e. down payment, up to the maturity date of the loan.

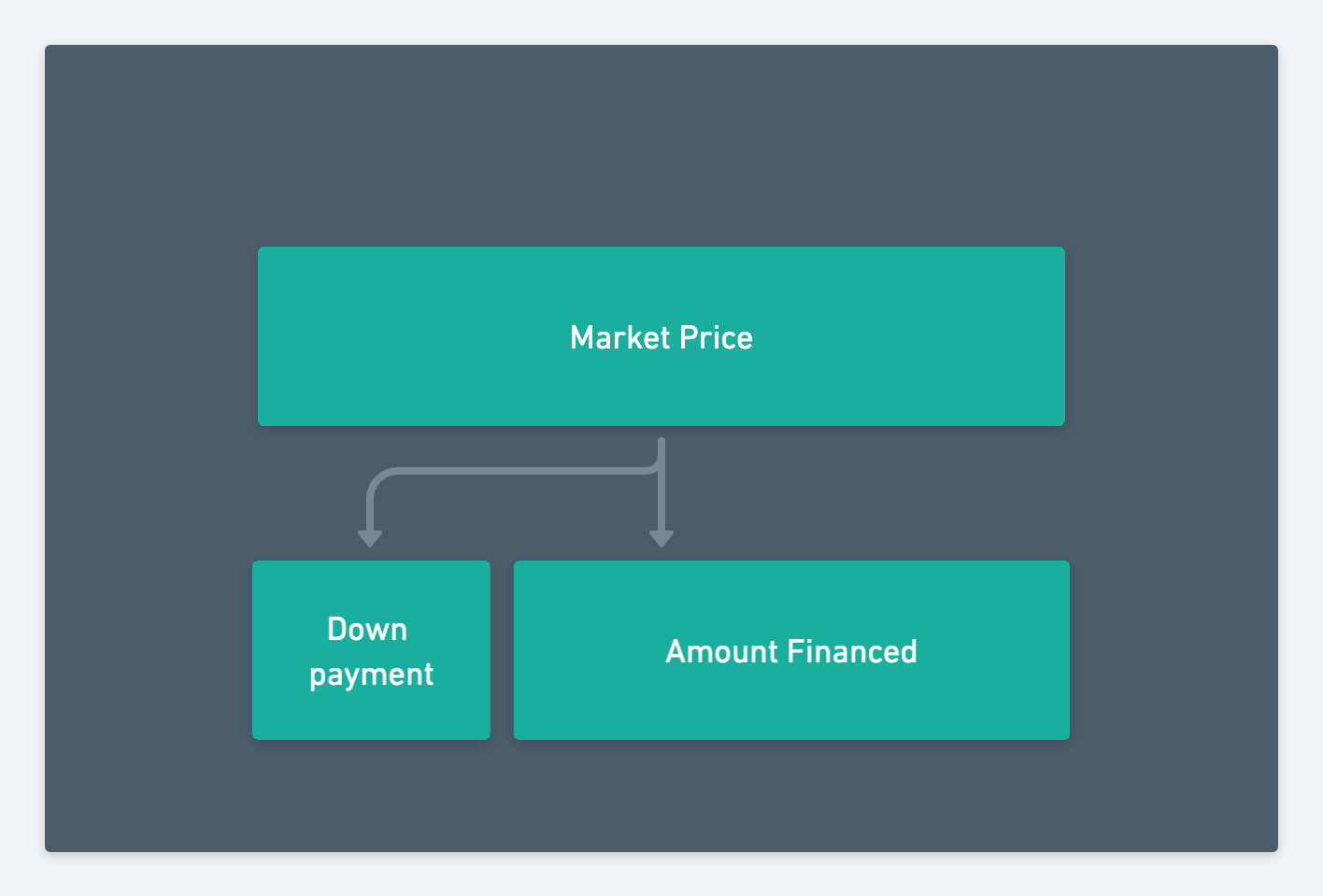

Split into Down payment and Amount Financed

{kind=link}

For a given market price of a product, we split that price into two parts, down payment and amount financed.

Down payment

It can either be a fixed price or a percentage of the market price. Also called equity, as the customer is paying this money in exchange for partial equity of the product.

Amount Financed

Market price minus down payment. This is the remaining amount that is going to be financed.

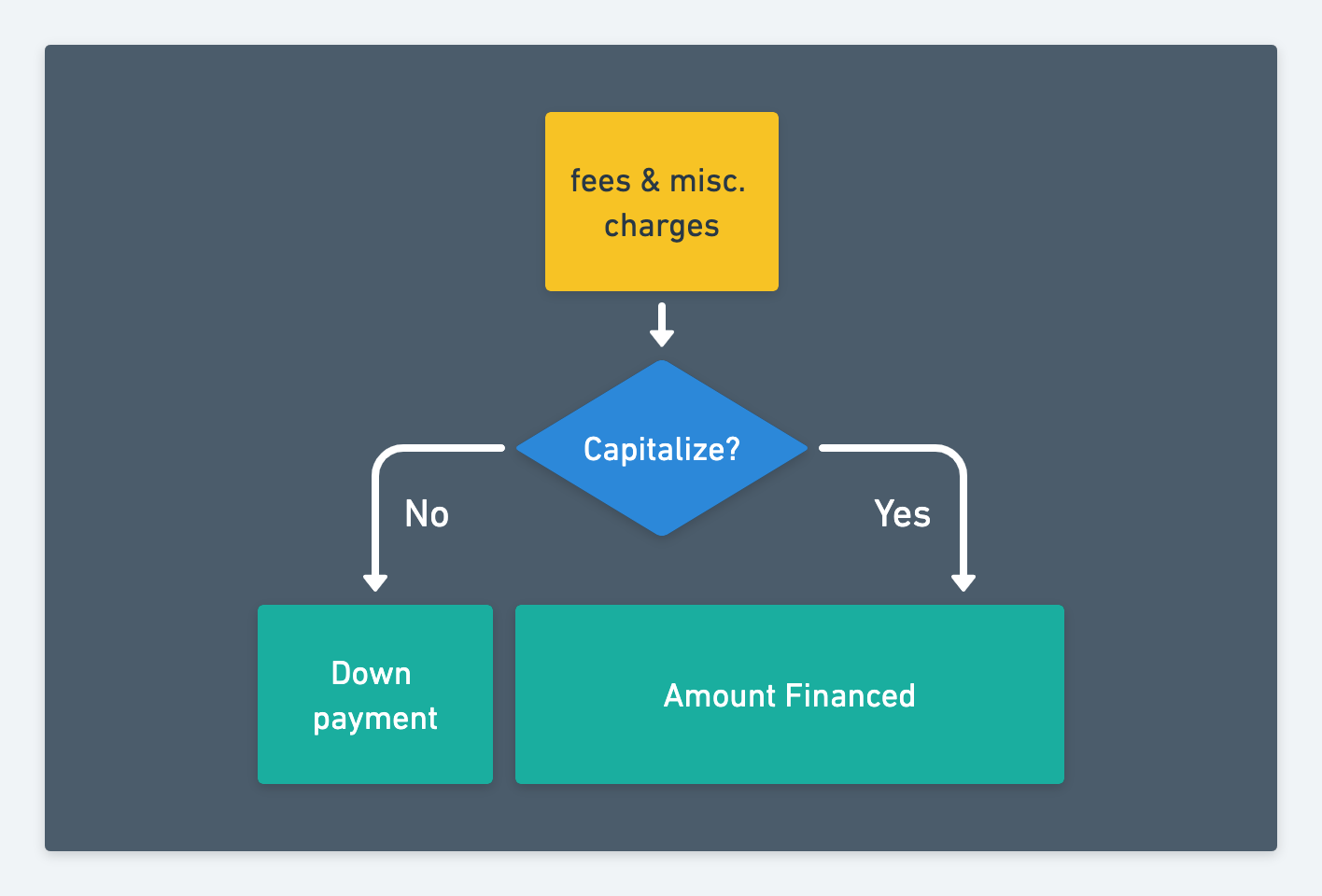

Capitalization

{kind=link}

After splitting the market price into down payment and amount financed, we now need to add profit and all other charges.

Now, the profit and charges can add up into either the down payment or the amount financed.

The process of adding up profit and charges into the amount financed is called capitalization (or EMI capitalization). A loan that adds the profit and charges into down payment is referred to as a non-capitalized loan.

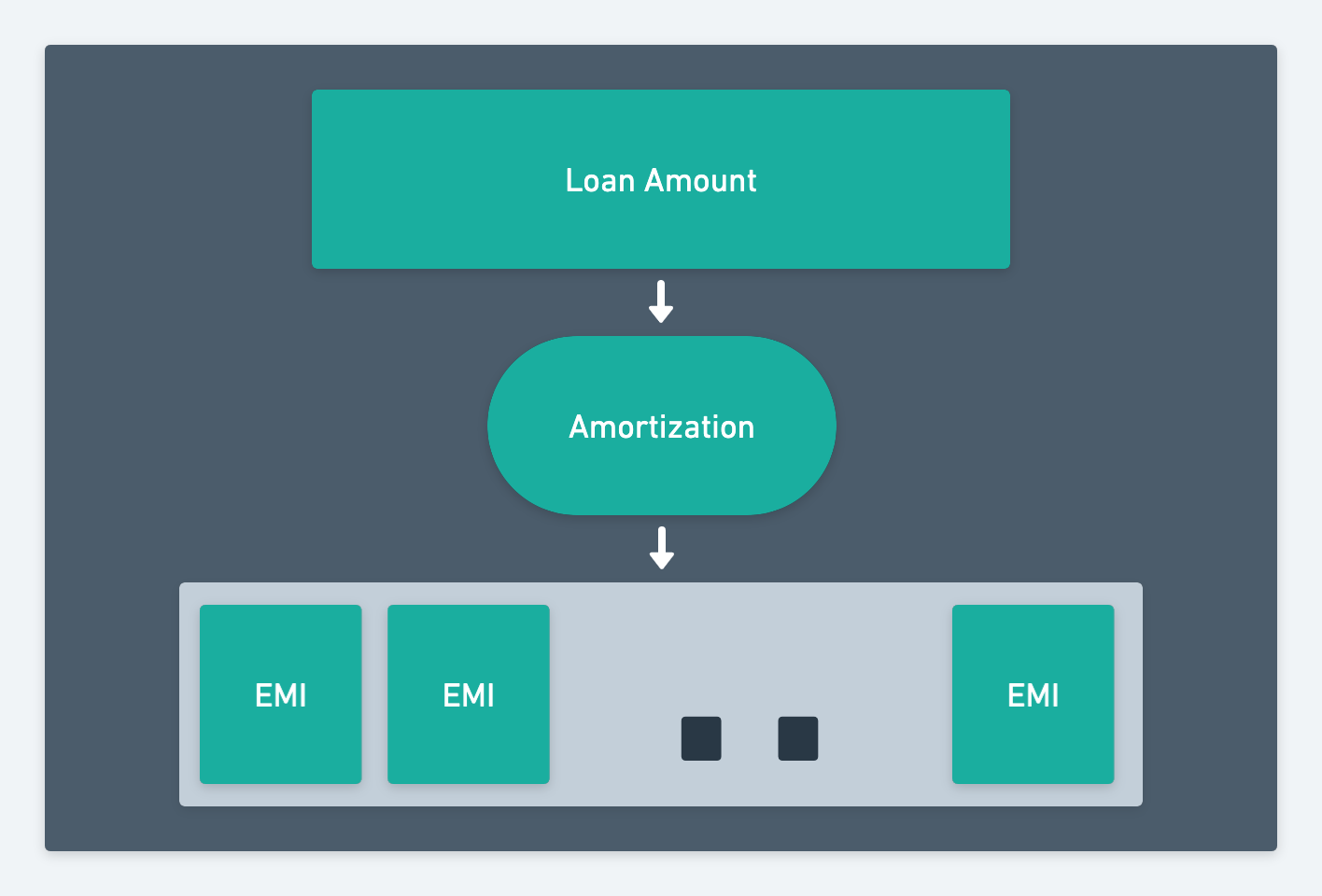

Amount Financed converted to repayments

{kind=link}

Once we have the entire loan amount, we can proceed to amortize the loan i.e. split it into multiple payments, called EMIs. It is also referred by other terms such as repayments, installments etc.

End Result

The EMI formula gives us fixed monthly payments.

The formula for calculating fixed payments being, (taken from investopedia):